How Selling Rental Property Affects Your Retirement Income

Selling rental property before retirement can simplify your finances by converting an asset to cash and ending landlord duties, but it can also trigger unexpected changes to your taxes, Social Security, Medicare costs, long term income, lifestyle, and financial control. Without a plan, you risk higher expenses and unproductive cash losing value to inflation.

Below is a clear breakdown of how a sale affects your retirement income and how to make the transition easier.

The Tax Hit That Surprises Most Sellers

When you sell rental property, the profit becomes taxable income. That profit includes appreciation and something called depreciation recapture. Both increase your modified adjusted gross income for the year of the sale.

Rental Property Tax

This is where the trouble starts. A large gain can:

Push you into a higher income tax bracket

Trigger depreciation recapture taxes

Expose you to the net investment income tax

Raise taxes on a portion of your Social Security benefits

These issues stack on top of each other. A strong market can make the profit look exciting, but the tax bill that follows can take a big share of the gain.

Get Your Free Guide to Real Estate Exit Strategies

How The Sale Affects Your Social Security Income

The sale itself does not change the amount of Social Security you receive. It does not reduce the benefit formula. But the income spike from the sale still affects your retirement income because of how the IRS taxes Social Security.

The IRS uses something called combined income. This includes your adjusted gross income, your interest income, and half your Social Security benefit. Once your combined income rises past certain levels, more of your Social Security benefit becomes taxable.

Up to 85 percent of your Social Security benefit becomes taxable once your income rises above the upper IRS threshold.

If a property sale pushes you above those thresholds, you keep less of your benefit that year.

The Medicare Premium Spike

This part catches retirees off guard. When your income jumps because of a property sale, Medicare may raise your Part B and Part D premiums two years later.

This increase is called IRMAA. The Social Security Administration looks back at your tax return from two years prior. If your income was higher because of a property sale, you may pay a monthly surcharge on your Medicare premiums for an entire year.

IRMAA can add several hundred dollars each month to your Medicare premiums after a property sale.

Many retirees overlook this because the surcharge appears two years after the income spike from the sale.

Get Your Free Guide to Real Estate Exit Strategies

Losing Rental Income in Retirement

Selling the property also means losing that monthly rent. If that rent covered expenses or reduced your need for withdrawals, you feel the difference immediately.

Some retirees underestimate how much that income supported their safety net. Others feel relieved to give it up because managing property became stressful. Both reactions are common.

What matters is this: you need a plan for replacing that income before you sell. Without one, your withdrawal rate may rise and shorten the life of your savings.

Liquidity Without a Plan Creates Risk

After the sale, you may end up with a large amount of cash. That feels safe. But cash loses value every year through inflation. Leaving sale proceeds idle exposes retirees to ongoing inflation loss, which reduces the real value of that cash every year it remains uninvested.

The solution is simple: treat the sale as part of your retirement plan, not an isolated event. Have a reinvestment plan before the property closes. Options may include income producing investments, inflation protected securities, or a diversified portfolio that matches your retirement timeline.

Timing Matters More Than Most People Realize

Timing matters more than most people expect. The year you choose to sell doesn’t just affect your income for a few months. It shapes your entire tax outcome. If you're planning to sell, don’t just ask how much you'll make. Ask when to sell to keep more of what you make.

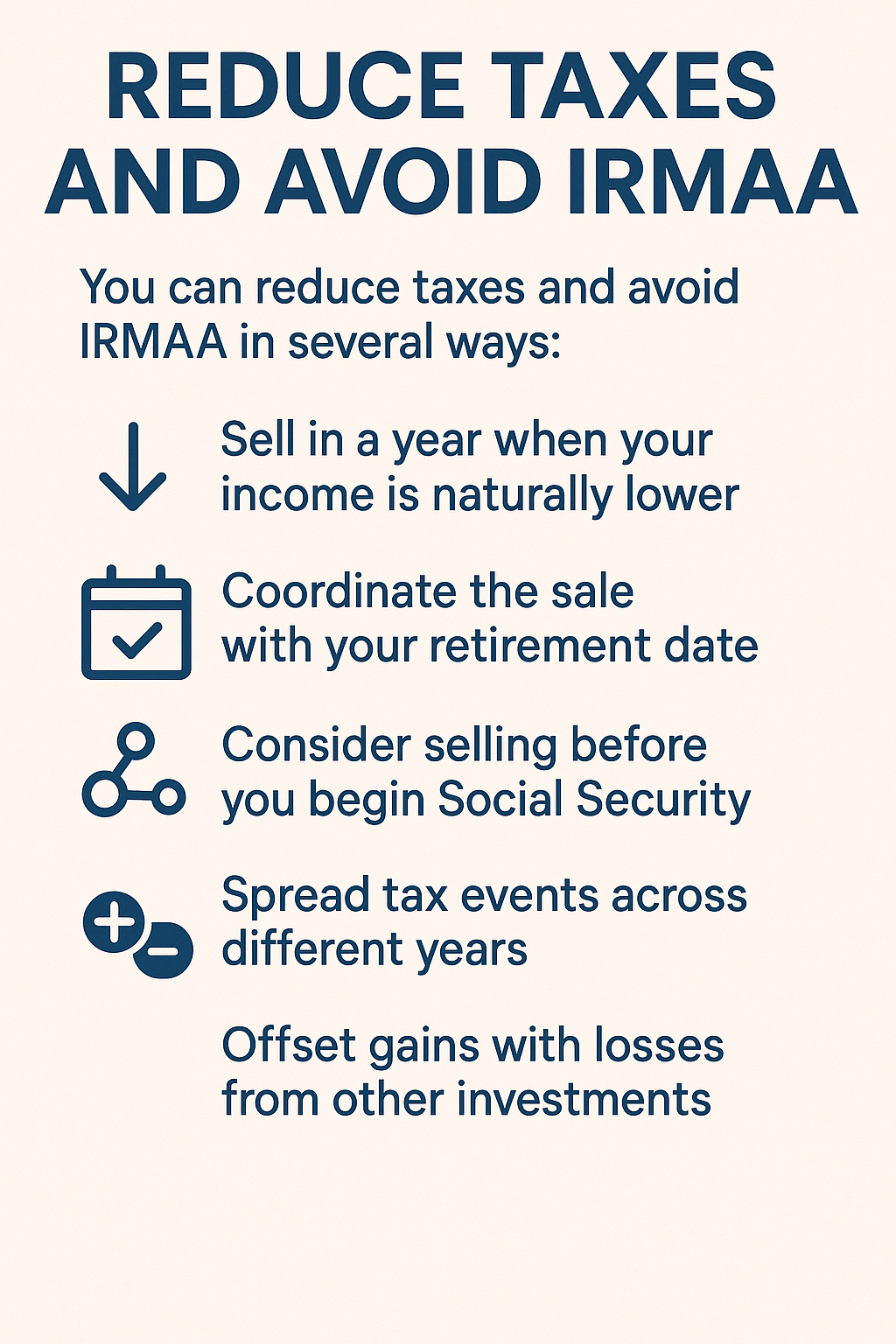

Reduce Taxes and avoid IRMAA

You can reduce taxes and avoid IRMAA in several ways:

Sell in a year when your income is naturally lower

Coordinate the sale with your retirement date

Consider selling before you begin Social Security

Spread tax events across different years

Offset gains with losses from other investments

A financial advisor can model these scenarios for you. The difference between selling in December versus January can be thousands of dollars in savings.

When Selling Strengthens Your Retirement Plan

Selling often makes sense if you want to simplify your life, reduce financial complexity, or shift to investments that are easier to manage. Many retirees choose to sell because they want more liquidity, less stress, or fewer moving parts in their finances.

If the property no longer fits your goals, or if managing tenants has become stressful, selling can give you more control and flexibility.

When Keeping the Property Works Better

Keeping the rental may help you if:

The income remains steady

The mortgage is paid off

You want an income stream that rises with inflation

You want to pass the property to children

You still enjoy being a landlord

These benefits can make a strong case for keeping the property, especially when the rental income stays steady and the management workload remains manageable. If the property supports your retirement goals and does not add stress, holding it may still be the right move.

The Emotional Side of the Decision

Most financial advice skips over the emotional weight tied to rental properties. But many owners stay invested not just for income. These places often hold family memories or mark a major financial milestone.

But retirement requires clarity. Ask yourself:

Does the property bring comfort or stress

Does the income help your plan or complicate it

Does the property support your goals or distract you

The best financial decision also needs to feel right emotionally.

How One Advisory Partners Helps You

Deciding whether to sell a rental property in retirement affects your taxes, income, Medicare costs, and long term financial plan. William Snider helps you make sense of these moving parts. With over 20 years in wealth management and trust services, he guides you through the tax impact of a sale, how it changes your income strategy, and the best way to reinvest the proceeds so your retirement stays on track.

You do not need to make this decision alone. If you want clear guidance on selling rental property or creating a stable retirement income plan, schedule a conversation with William Snider at ONE Advisory Partners. He serves clients nationwide and can help you choose the path that strengthens your retirement.

Book a call with William Snider.

Get Your Free Guide to Real Estate Exit Strategies

The Bottom Line

Selling a rental property affects your retirement income in several ways. It raises your taxable income, it can raise Medicare premiums two years later, and it can change how much of your Social Security benefit becomes taxable. You also lose rental income and face inflation risk if you leave the cash sitting in a bank account.

A thoughtful plan can help you avoid the tax spike, protect your Medicare costs, and get the proceeds invested in a way that supports your long term goals. The decision to sell is personal. The key is to match the financial outcome with the retirement lifestyle you want.

FAQs About Rental Property and Retirement Income

Does selling rental property reduce my Social Security benefit

No. The sale does not lower the benefit amount you receive. It can only affect how much of your benefit becomes taxable for that year.

Can selling rental property increase my Medicare premiums

Yes. A higher income in the year of the sale can trigger IRMAA, which raises Medicare premiums two years later.

Will I lose rental income if I sell

Yes. Once you sell, that monthly cash flow stops, so you need a plan to replace it.

Is depreciation recapture part of the tax bill

Yes. The IRS taxes the depreciation you claimed while owning the property, which increases your taxable income.

Should I reinvest the proceeds

Yes. Holding cash means losing value over time to inflation. To protect your money and keep it working for you, you need a clear investment plan in place after the sale.

Is there a best time to sell

The best time depends on your income levels, retirement date, and tax situation. Timing can reduce taxes and prevent IRMAA.

Reference

Beattie, A. (2024, December 02). How to Limit Taxes When Selling Your Rental Property. Investopedia. Retrieved from https://www.investopedia.com/articles/mortgages-real-estate/08/rental-property.asp

Internal Revenue Service. (2008, February). Like-Kind Exchanges Under IRC Section 1031 (FS-2008-18). Retrieved from https://www.irs.gov/pub/irs-news/fs-08-18.pdf

Investopedia Staff. (2015, May 15). Are Rental Properties Worth Investing In? Pros, Cons & Expert Tips. Investopedia. Retrieved from https://www.investopedia.com/articles/investing/051515/pros-cons-owning-rental-property.asp

Bay Property Management Group. (2023, February 14). Should You Sell Your Investment Before Retirement? Retrieved from https://www.baymgmtgroup.com/blog/sell-your-investment-before-retirement/