IRS Tax Guide for People With Disabilities in 2025

Living with a disability often comes with added financial responsibilities. Medical care, assistive technology, transportation, and long term planning can all affect your budget. The good news is that the IRS provides several tax benefits that may help reduce your tax liability if you qualify.

Although this guide explains the IRS rules that apply to 2025 federal tax returns, several disability planning rules have changed for 2026. This article highlights the 2025 tax provisions while noting important changes that may affect future planning.

Tax Benefits Available for People With Disabilities

The federal tax code includes several tax breaks that may help people with disabilities and their families lower their tax bill. Depending on your situation, you may qualify for tax free disability benefits, deductions for certain medical expenses, tax credits, employer provided benefits, and tax advantaged savings through an ABLE account.

The IRS explains these rules in Publication 907, which covers the tax benefits available to eligible individuals with disabilities and their caregivers. Understanding how these rules apply to your situation can help you avoid reporting mistakes and identify deductions or credits you may be eligible to claim when filing your 2025 federal tax return.

Which Disability Income Is Taxable?

Not every payment you receive because of a disability is taxed the same way. Some benefits are fully taxable, some are partially taxable, and others are completely excluded from federal income tax.

For example, disability pensions paid by an employer are generally taxable until you reach your minimum retirement age. After that, the payments are usually taxed as regular pension income. If you receive only Social Security Disability Insurance (SSDI) benefits, they are often not taxable. However, if you have additional income, part of your Social Security benefits could become taxable depending on your filing status and total income.

Read: Are You Missing Key Family Tax Opportunities?

Which Disability Benefits Are Not Taxable?

Many disability related payments are excluded from federal income tax. Knowing which benefits are taxable and which are not can help you report your income correctly and avoid paying more tax than necessary.

Examples of nontaxable disability related payments include:

Supplemental Security Income (SSI)

Veterans Affairs (VA) disability compensation and pension benefits

Workers' compensation benefits for an occupational injury or sickness

Compensatory damages for physical injury or physical sickness

Certain no fault insurance disability benefits for lost income or earning capacity

Public welfare payments, such as benefits due to blindness

Certain military and government disability pensions

Qualified long term care insurance benefits

Medical Expense Deductions

Medical expenses can become a significant part of your annual budget. If you itemize deductions, you can generally deduct qualified medical and dental expenses that exceed 7.5% of your adjusted gross income (AGI).

Qualified medical expenses may include:

Wheelchairs

Hearing aids

Artificial limbs

Eyeglasses

Guide dogs or other service animals that assist a person with a physical disability

Home accessibility improvements made for medical purposes

Transportation for qualified medical care

Qualified long term care insurance premiums, subject to IRS limits

Some home improvements, such as installing wheelchair ramps, may qualify as medical expenses if their primary purpose is medical care. If the improvement increases the value of your home, only part of the cost may be deductible.

Also read: How Social Security Works After Your Spouse Dies

Impairment Related Work Expenses

Some people with disabilities pay for goods or services that allow them to perform their jobs. In certain situations, these costs may qualify as impairment related work expenses.

The IRS allows qualifying impairment related work expenses to be deducted as business expenses rather than medical expenses. To qualify, the expenses must be ordinary and necessary, required for you to do your work satisfactorily, not used for personal activities except incidentally, and not covered under other income tax laws. Unlike medical expenses, these deductions are not subject to the 7.5% adjusted gross income limitation.

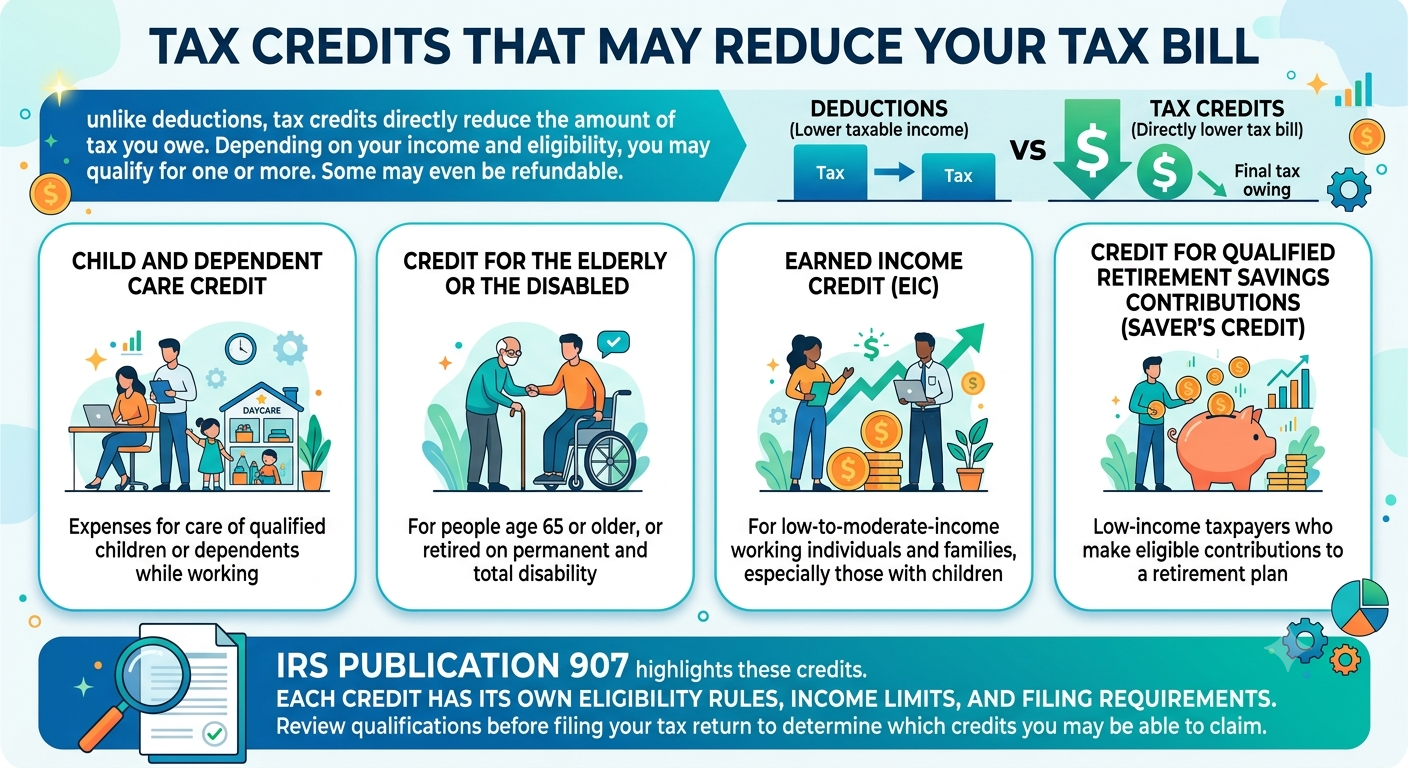

Tax Credits That May Reduce Your Tax Bill

Unlike deductions, tax credits directly reduce the amount of tax you owe. Depending on your income and eligibility, you may qualify for one or more tax credits that can lower your tax bill. Some credits may even be refundable.

IRS Publication 907 highlights the following tax credits:

Child and Dependent Care Credit

Credit for the Elderly or the Disabled

Earned Income Credit (EIC)

Credit for Qualified Retirement Savings Contributions (Saver's Credit)

Each credit has its own eligibility rules, income limits, and filing requirements. Reviewing the qualifications before filing your tax return can help you determine which credits you may be able to claim.

What Is an ABLE Account?

An ABLE account is a tax favored savings account created under the Stephen Beck, Jr. Achieving a Better Life Experience (ABLE) Act. It allows eligible individuals with a disability or who are blind to save money for qualified disability expenses. An ABLE account is generally disregarded when determining eligibility for Supplemental Security Income (SSI) and certain other means tested federal programs. However, SSI has a special rule for larger balances. The first $100,000 in an ABLE account is excluded for SSI resource purposes. Amounts above that threshold count toward the SSI resource limit. If your countable resources exceed the limit because your ABLE account balance is over $100,000, your SSI cash benefits are suspended until the balance falls below the applicable threshold. Medicaid eligibility generally continues during the suspension.

Qualified disability expenses are costs related to maintaining or improving your health, independence, or quality of life. They may include education, housing, transportation, employment training and support, assistive technology, health, prevention and wellness, financial management, administrative services, legal fees, oversight and monitoring, and funeral and burial expenses. Investment earnings generally grow tax free when distributions are used to pay qualified disability expenses.

Who Can Open an ABLE Account?

Beginning January 1, 2026, you may qualify to open an ABLE account if your blindness or disability occurred before age 46. This expanded eligibility results from the ABLE Age Adjustment Act, allowing millions more Americans with disabilities to qualify for an ABLE account.

To be eligible, you must either receive disability benefits under Title II or Title XVI of the Social Security Act or meet the disability certification requirements of your state's qualified ABLE program.

If you're unable to establish the account yourself, it may be opened by an agent under a power of attorney. If there is no agent, a conservator or legal guardian, spouse, parent, sibling, grandparent, or a representative payee appointed by the Social Security Administration may establish the account on your behalf. However, only you, as the designated beneficiary, can have an interest in the account during your lifetime.

2025 ABLE Account Contribution Limits

For 2025, the annual ABLE account contribution limit is $19,000. Certain employed beneficiaries may be eligible to contribute an additional amount based on their compensation, provided they meet the IRS requirements.

Each state's ABLE program also has a cumulative account balance limit based on its 529 qualified tuition program. If contributions cause an account to exceed that limit, the state ABLE program generally returns the contributions that created the excess and notifies the beneficiary.

What Happens If You Contribute Too Much?

Contributing more than the annual IRS limit can result in additional taxes. If your ABLE account receives excess contributions, both the excess amount and any earnings on those contributions must be returned by the due date of your federal income tax return, including extensions.

If the excess contributions and earnings are not returned by the deadline, you may be subject to a 6% excise tax. Monitoring your contributions throughout the year can help you avoid unnecessary taxes and preserve the tax advantages of your ABLE account.

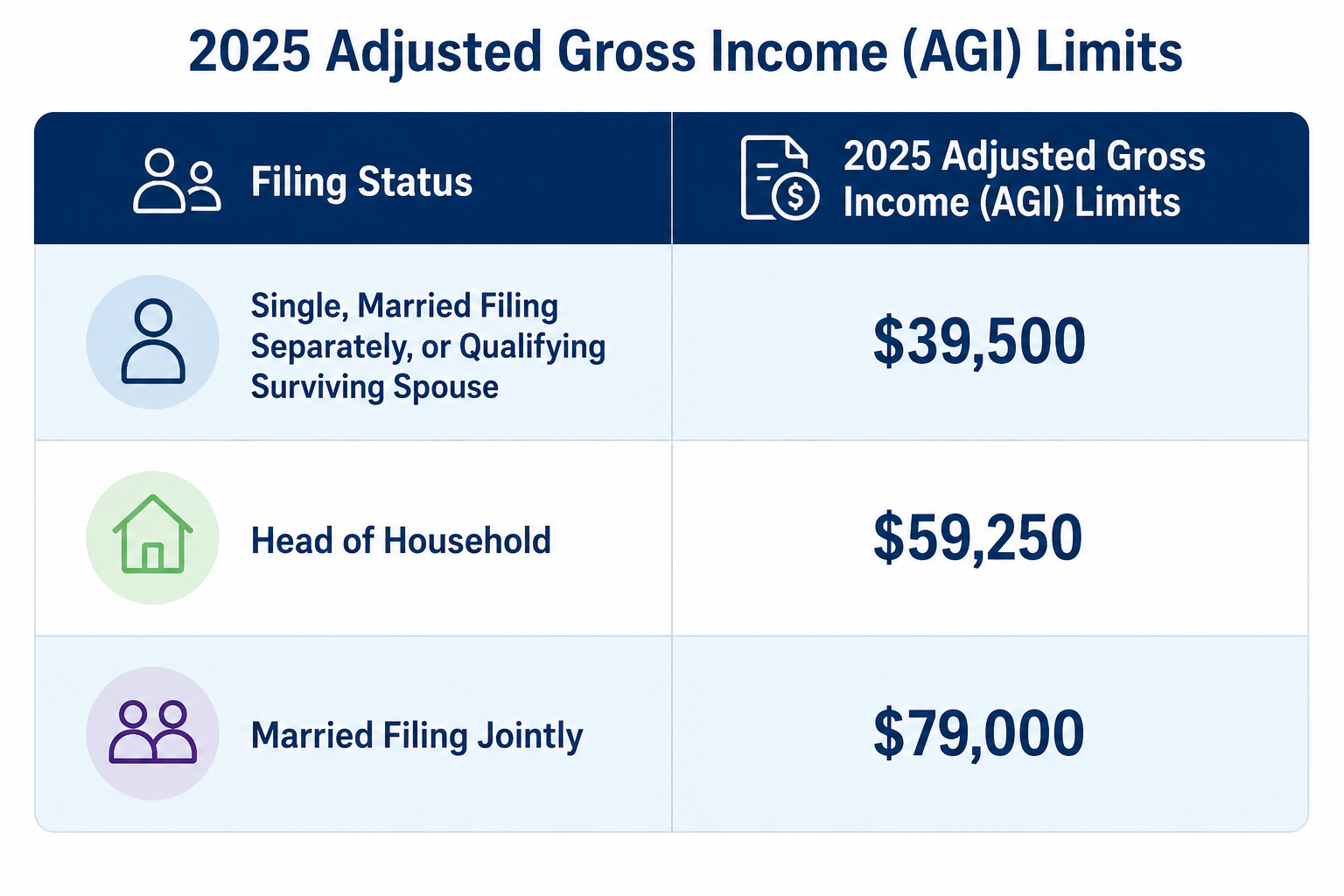

Saver's Credit for ABLE Contributions

Eligible contributions to an ABLE account may qualify for the Credit for Qualified Retirement Savings Contributions, commonly known as the Saver's Credit. To qualify, you must meet the IRS eligibility requirements, including income limits and other qualifications.

For 2025, the modified adjusted gross income (MAGI) limits are:

2025 Adjusted Gross Income (AGI) Limits

Although many publications refer to modified adjusted gross income (MAGI), the Saver's Credit generally uses adjusted gross income (AGI), with only limited adjustments in certain situations.

Planning Ahead: Beginning with tax year 2027, the SECURE 2.0 Act replaces the Saver's Credit with the federal Saver's Match. Instead of receiving a tax credit, eligible taxpayers may receive a federal matching contribution of up to $1,000 deposited directly into their retirement account. Taxpayers should review the updated rules before making future retirement or ABLE contribution decisions.

Dependent Care Benefits

If your employer provides dependent care benefits through a qualified plan, you may be able to exclude those benefits from your taxable income if you meet the IRS requirements. These benefits can help cover the cost of caring for a qualifying child under age 13, a disabled spouse, or another qualifying dependent while you work.

Dependent care benefits may include payments made directly to you or your care provider, the fair market value of care in an employer provided or sponsored daycare facility, or pre tax contributions to a dependent care flexible spending arrangement (FSA). The amount you can exclude depends on your qualifying expenses, earned income, your spouse's earned income, and the amount of benefits you receive.

Household Employer Rules

Many families hire caregivers, personal assistants, or housekeepers to help support a loved one with a disability. Depending on the working relationship, you may be considered a household employer under IRS rules.

If you control what work is done and how it is performed, the worker is generally considered your employee, and you may have employment tax responsibilities. If the worker is employed through an agency that controls the work, the agency is generally responsible for those obligations. Understanding these rules can help you avoid unexpected tax responsibilities and filing issues.

Tax Benefits for Businesses

IRS Publication 907 highlights several tax incentives that encourage businesses to improve accessibility and expand employment opportunities for people with disabilities.

These incentives include:

Disabled Access Credit

Deduction for costs of removing barriers to the disabled and the elderly

Work Opportunity Credit for hiring eligible individuals from targeted groups, including certain vocational rehabilitation referrals with disabilities

Business owners should review the eligibility requirements before claiming these incentives, as each credit or deduction has specific qualification rules and reporting requirements.

Keep Good Records for Tax Time

Claiming disability related tax benefits often requires accurate records and the appropriate IRS forms. Depending on your situation, you may need documentation for medical expenses, impairment related work expenses, dependent care benefits, or ABLE account contributions when preparing your federal tax return.

If you receive forms such as Form W2, Form 1099 QA, or Form 5498 QA, review them carefully and keep them with your tax records. If you have questions about your eligibility for a deduction, credit, or exclusion, the IRS recommends reviewing the applicable instructions and publications or seeking assistance from a qualified tax professional.

How a Virtual Family Office Can Help

Taxes are only one part of your financial picture. If you're living with a disability or helping a family member plan for the future, your decisions about income, healthcare costs, retirement savings, and estate planning often work together. Looking at each piece separately can lead to missed opportunities.

A Virtual Family Office takes a broader approach by coordinating tax planning with investment management, retirement income strategies, estate planning, and long term financial goals. This can help you make informed decisions while adapting to changes in tax laws and your personal circumstances.

Read: What Is Virtual Family Office and Why More Families Are Moving to It

Bottom Line

The IRS Tax Guide for People With Disabilities for the 2025 tax year provides valuable information about taxable income, deductions, tax credits, and ABLE accounts. If you're planning in 2026 and beyond, remember that ABLE account eligibility has expanded to individuals whose disability began before age 46, creating new planning opportunities for many families.

If you want to see how disability related tax planning fits into your retirement, investment, and estate strategy, the advisors at ONE Advisory Partners can help. Our Virtual Family Office brings your financial, tax, and long term planning together, giving you a clearer path toward protecting your future and your family's financial well being.

Frequently Asked Questions

Are Social Security disability benefits taxable?

If Social Security benefits are your only source of income, they are generally not taxable. However, if you receive other income, part of your Social Security benefits may be taxable depending on your filing status and total income. Supplemental Security Income (SSI) is not taxable.

What is the ABLE account contribution limit for 2025?

The annual ABLE account contribution limit for 2025 is $19,000. Certain employed beneficiaries may be eligible to contribute an additional amount if they meet the IRS requirements.

Can I deduct medical expenses?

Yes. If you itemize deductions, you may deduct qualified medical expenses that exceed 7.5% of your adjusted gross income. Eligible expenses may include wheelchairs, hearing aids, guide dogs, accessibility improvements, transportation for medical care, and other qualified medical costs.

Can I claim a tax credit if I have a disability?

Possibly. Depending on your income and circumstances, you may qualify for the Credit for the Elderly or the Disabled, the Earned Income Credit, the Child and Dependent Care Credit, or the Saver's Credit for qualifying retirement or ABLE account contributions.

Are VA disability benefits taxable?

No. Disability compensation and many other benefits paid by the Department of Veterans Affairs are excluded from federal taxable income.

Can businesses receive tax incentives for improving accessibility?

Yes. Eligible businesses may qualify for the Disabled Access Credit, a deduction for costs of removing barriers to the disabled and the elderly, or the Work Opportunity Credit for hiring eligible individuals from targeted groups, including certain vocational rehabilitation referrals with disabilities.

References

Internal Revenue Service. (2026). Publication 907 (2025), Tax Highlights for Persons With Disabilities. Retrieved fromhttps://www.irs.gov/publications/p907

Social Security Administration. (2026). Spotlight on Achieving a Better Life Experience (ABLE) Accounts. Retrieved fromhttps://www.ssa.gov/ssi/spotlights/spot-able.html

Internal Revenue Service. (2026). Publication 502, Medical and Dental Expenses. Retrieved fromhttps://www.irs.gov/publications/p502

Internal Revenue Service. (2026). Publication 525, Taxable and Nontaxable Income. Retrieved fromhttps://www.irs.gov/publications/p525

Internal Revenue Service. (2026). Publication 596, Earned Income Credit. Retrieved fromhttps://www.irs.gov/publications/p596

Internal Revenue Service. (2026). Publication 926, Household Employer's Tax Guide. Retrieved fromhttps://www.irs.gov/publications/p926