What Does Fee-Only Financial Advice Really Mean?

When you look for a financial advisor, "fee-only" is one of the most common terms you will encounter. While it sounds straightforward, it is frequently misunderstood by investors. Fee-only is not a description of advice quality or an advisor's intentions. Instead, it is a specific method of compensation that plays a critical role in shaping the financial advice you receive.

Understanding how an advisor is paid helps you evaluate potential conflicts of interest and decide which relationship is right for your family.

The Three Basic Compensation Models

Most financial advisors are compensated in one of three ways: commission-based, fee-based, or fee-only. Although these terms are often used interchangeably, they describe materially different business models.

1. Commission-Based Advisors

Commission-based advisors are paid when they sell financial products, such as mutual funds, annuities, or insurance policies. Their compensation depends on the type of product sold, the amount you invest, and the frequency of your transactions.

Because their income is tied directly to product sales, this model creates an inherent conflict of interest. An advisor may be financially rewarded for recommending certain products over others. While many of these advisors aim to serve clients well, the structure makes it difficult to separate objective advice from a sales pitch.

2. Fee-Based Advisors: The Hybrid Approach

"Fee-based" does not mean "fee-only". Under this hybrid structure, an advisor charges an ongoing advisory fee but may also receive commissions from selling products. This can make it difficult for investors to determine when advice is fully objective and when compensation is influencing a recommendation.

3. Fee-Only Financial Advice

Fee-only advisors are compensated solely by their clients. They do not receive commissions, referral fees, or any other form of product related compensation. The defining characteristic of this model is not how the fee is calculated, whether it is hourly, a flat fee, or a percentage of assets, but that the client is the only source of compensation.

Read: What Does A Virtual Family Office Do And Who Actually Needs One?

Why the Distinction Matters for Your Wealth

For families managing meaningful wealth, the difference goes beyond terminology. It shapes every aspect of the relationship, from the products you are shown to whether your advisor's financial interests are truly aligned with yours.

A conflict of interest exists whenever a recommendation benefits the advisor financially in a way that might not benefit the client. In financial services, these conflicts are particularly influential because they are ongoing and often invisible to the investor. They affect which options are presented and which are emphasized.

Fee-only advisors are structurally positioned to be more objective because their compensation does not depend on product selection. Their pay does not increase if you purchase a specific financial product. As a result, they are free to recommend lower-cost options, evaluate alternatives openly, and even advise you when not to take action.

Also read: What Is Virtual Family Office and Why More Families Are Moving to It

Who Defines "Fee-Only"?

Because terminology is not always used consistently, it is important to know who sets the standards. The most widely accepted definition comes from the National Association of Personal Financial Advisors (NAPFA).

NAPFA is a nonprofit organization with strict standards. To qualify for membership, advisors must:

Accept no commissions of any kind.

Be paid exclusively by their clients.

Undergo review by a membership committee to confirm compliance.

NAPFA membership serves as a credible, independent third-party credential rather than just a marketing claim. Additionally, fee-only advisors who are Registered Investment Advisers (RIAs) are legally required to act as fiduciaries, meaning they must recommend what is in your best interest.

Assets Under Management (AUM) vs. Flat Fees

Within the fee-only world, there are different ways to pay your advisor. About 92% of advisors use the traditional Assets Under Management (AUM) model.

AUM Model: You pay a percentage of your portfolio's value each year. For example, the industry average fee on a $3 million account is roughly 0.88%, which equals $26,400 per year.

Flat-Fee Model: This approach is growing in popularity among retirees. A flat-fee advisor charges a set, transparent dollar amount for services regardless of portfolio size.

The AUM model has come under scrutiny because as a portfolio grows, the fee can become disproportionate to the work being done. A 1% fee on $500,000 may be fair for good advice, but a $50,000 annual fee on a $5 million portfolio can feel excessive. Flat-fee models offer predictable pricing that helps reduce anxiety about hidden or escalating costs.

What This Looks Like in Practice

A fee only structure removes the incentive to favor products that generate higher compensation. This allows the advisor to focus on complex financial situations, such as business transitions, estate coordination, and multi generational planning, without the bias of product sales.

However, structure alone is not a guarantee of quality. Expertise, experience, and depth of service still vary widely among fee-only firms. The compensation model is simply a starting condition that ensures your advisor is working for you, not a product manufacturer.

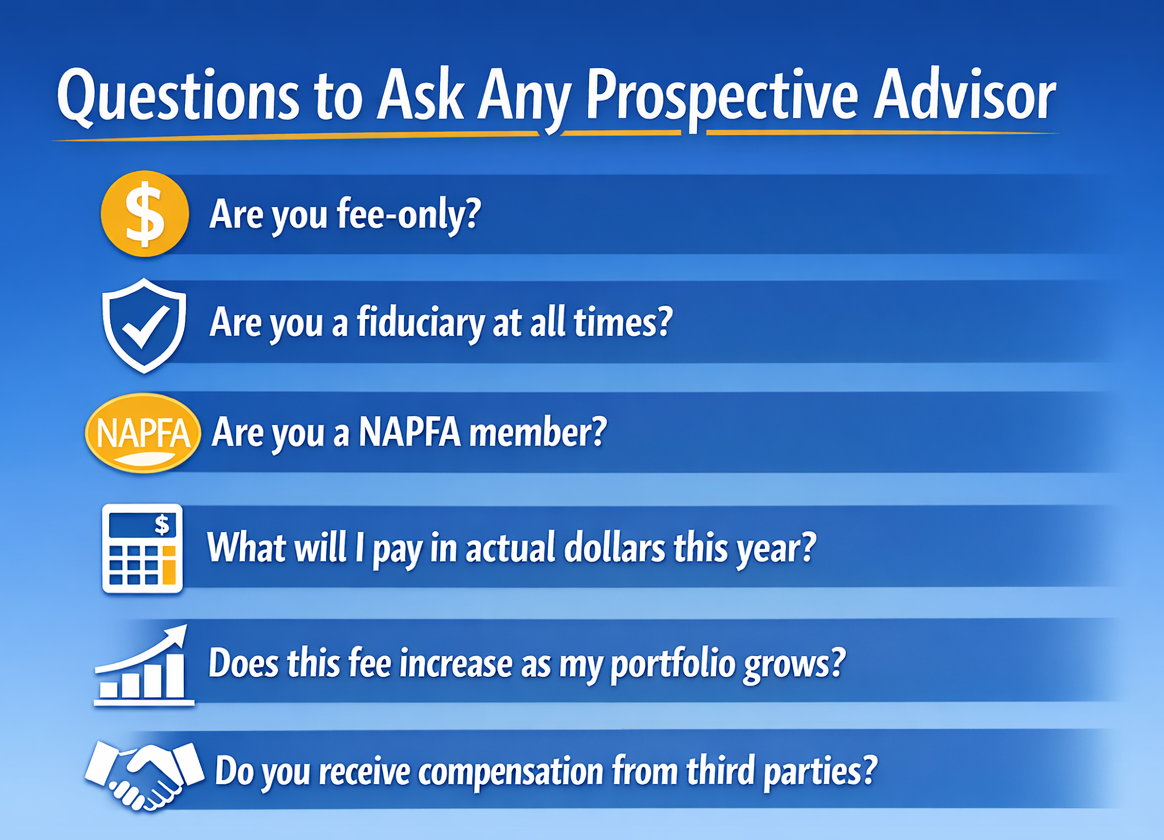

Questions to Ask Any Prospective Advisor

Before engaging a financial advisor, use these questions to verify their status and understand what you are paying for:

Are you fee-only? Specifically, ask if they are fee-only rather than fee-based.

Are you a fiduciary at all times? Ensure they are fiduciaries for all services, not just some.

Are you a NAPFA member? This confirms a verified, non-self-reported standard.

What will I pay in actual dollars this year? Ask for a clear annual dollar amount rather than just a percentage.

Does this fee increase as my portfolio grows? Determine if they use a flat fee or an AUM model.

Do you receive compensation from third parties? This includes referral fees or revenue sharing.

A Different Approach to Transparency

Most investors are used to a model where their advisor’s pay is a mystery or tied exclusively to the size of their portfolio. We believe there is a better way to structure a professional relationship. Our model at ONE Advisory Partners is designed to be straightforward and clear.

The Structure

Annual Membership Fee: Starting at $10,000. This provides you with a dedicated team for comprehensive financial planning, retirement guidance, tax strategy and preparation, and estate planning coordination. It is a predictable cost for professional oversight.

Asset-Based Fee: 0.35% on managed assets. This is used to cover the specific costs of direct investment management. By keeping this rate significantly lower than the common 1% industry average, more of your market growth stays in your accounts.

The Results of This Model

Clarity: You know exactly what you are paying in dollars, not just percentages.

Objectivity: Because we do not earn commissions, our guidance is based on your goals rather than product sales.

Scalability: As your wealth increases, your costs do not necessarily balloon at the same rate, which can lead to meaningful savings over time.

This approach is intended to provide a professional partnership where the value is visible and the incentives are aligned with your long-term success.

Frequently Asked Questions (FAQ)

What is the difference between fee-only and fee-based? Fee-only advisors are paid only by their clients and never earn commissions. Fee-based advisors charge a fee but may also earn commissions from products they sell.

Does fee-only mean lower cost? Not necessarily. Fee-only advisors charge for advice directly, making the cost visible. Commission-based models may appear free but embed costs in the products themselves, often making them harder to see.

What is NAPFA, and why does it matter? NAPFA is the National Association of Personal Financial Advisors. It maintains the strictest definition of fee-only compensation and monitors members to ensure they never accept commissions.

Is a fiduciary always a fee-only advisor? No. Fiduciary is a legal obligation to act in the client's best interest. Some fiduciaries still earn commissions but must disclose the conflict. Fee-only advisors who are fiduciaries align both the legal obligation and the pay structure in the client's favor.

How do I verify an advisor's fee-only status? You can search for members at napfa.org or review an advisor’s Form ADV through the SEC’s Investment Adviser Public Disclosure database.

Does a flat fee always save me money? Not always. For example, a $10,000 flat fee on a $750,000 portfolio is actually more expensive than a 1% AUM fee ($7,500). It is important to run the math for your specific portfolio size.

The Bottom Line

How your advisor is paid affects the advice you receive, and a fee-only structure removes a major source of bias, but what matters most is how everything is coordinated. At ONE Advisory Partners, the focus is on aligning investments, taxes, retirement income, and estate strategy into one clear plan, so if you want a more connected approach to your finances, start with a conversation.