What To Look For In A Fiduciary Retirement Advisor

Choosing a fiduciary retirement advisor is one of the most important financial decisions you will make. Not all advisors who claim to act in your best interest actually do.

This article explains what truly matters when evaluating a fiduciary retirement advisor and how to tell the difference before you commit.

What Does Fiduciary Really Mean?

A fiduciary retirement advisor is legally required to act in your best interest when providing financial advice. This duty goes beyond good intentions and applies to recommendations, implementation, and ongoing monitoring.

Many advisors use the word fiduciary loosely. What matters is whether they are obligated to that standard at all times and whether it is documented clearly in writing.

Are They A Fiduciary At All Times?

Some advisors act as fiduciaries only in certain situations, such as financial planning, but not when selling products. This creates confusion and potential conflicts.

You should confirm that fiduciary duty applies 100% of the time, not selectively. If an advisor cannot answer this clearly or avoids putting it in writing, that is a red flag.

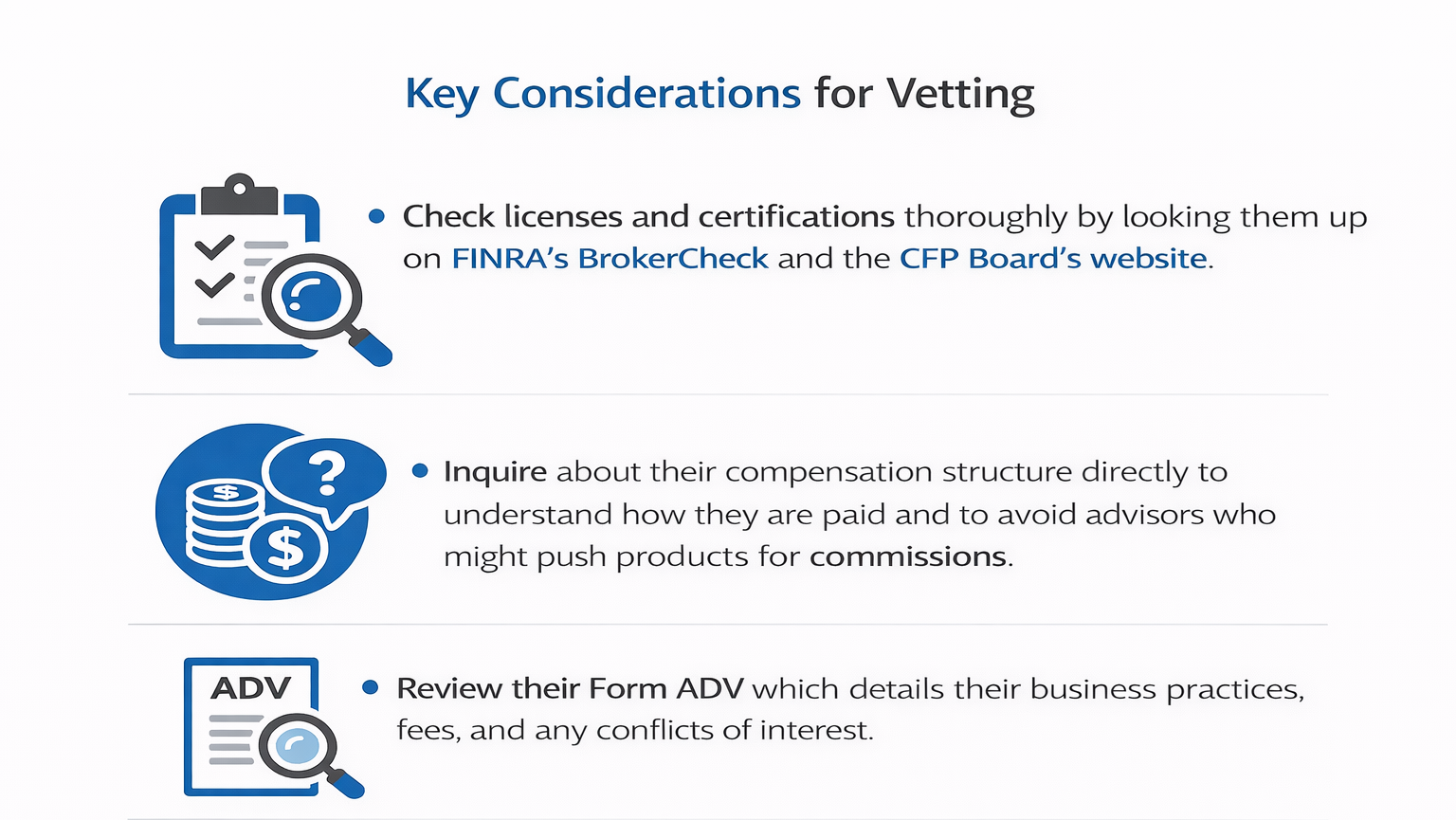

How Is The Advisor Actually Paid?

Compensation structure directly affects advice. Fee-only advisors are paid only by their clients and do not earn commissions or sales related compensation.

Fee-based advisors may charge fees while also earning commissions from products. This creates incentives that can influence recommendations, even if unintentionally.

What Credentials And Experience Matter Most?

Credentials help establish baseline competence, but not all designations carry the same weight. A Certified Financial Planner CFP® is held to enforceable fiduciary and planning standards.

Beyond credentials, look for experience working with people in retirement or near retirement. Retirement income planning, tax strategy, and benefit coordination require specific expertise.

Do They Specialize In Retirement Planning?

Retirement planning involves far more than managing investments. It requires coordinating income, taxes, Social Security, risk, and long-term planning decisions.

An advisor who focuses only on portfolio performance may overlook factors that directly impact retirement sustainability and cash flow.

How Do They Explain Risk And Tradeoffs?

A fiduciary advisor should explain risk clearly and without jargon. This includes market risk, inflation risk, and the role of bonds in a retirement portfolio.

If an advisor cannot clearly explain tradeoffs or downside scenarios, they may not be prepared to guide long-term retirement decisions responsibly.

What Is Their Planning Process?

Strong fiduciary advisors follow a structured, documented planning process. This process should include understanding your full financial picture, analyzing alternatives, and presenting clear recommendations.

You should know what happens after the plan is created. Ongoing monitoring, updates, and accountability are part of fiduciary responsibility.

How Transparent Are Fees And Services?

You should understand exactly what you pay and what services you receive. Fees should be clearly disclosed, easy to explain, and consistent with the scope of work.

Complex or vague fee explanations often hide conflicts. Transparency is a core signal of fiduciary alignment.

How Do You Verify An Advisor’s Background?

You do not need to rely on trust alone. Public databases allow you to verify licenses, disclosures, and disciplinary history.

A fiduciary advisor should encourage you to review their background and be comfortable answering questions about it.

Why Work With A Fiduciary At All?

Working with a fiduciary means advice is provided under a legal obligation to place your interests first. This standard helps reduce conflicts that can arise from commissions, sales incentives, or product driven recommendations.

A fiduciary relationship also supports clearer accountability. Advice must be based on your goals, constraints, and long term planning needs rather than what benefits the advisor or their firm. This framework helps create a more transparent and structured planning relationship, especially for retirement decisions that are difficult to reverse.

What Makes ONE Advisory Partners Different From Other Financial Advisors?

We operate as a fee-only fiduciary. Our compensation is based on a clearly defined planning fee, and we do not receive commissions, product sales compensation, or investment-based incentives. This structure is intended to help limit conflicts of interest and support a planning-focused advisory relationship.

Our services are structured around comprehensive retirement planning rather than standalone investment management. Fees are disclosed in advance and are associated with ongoing planning services, which may include retirement income considerations, tax coordination, risk management, and long-term planning support. Clients receive clarity around fees, services, and how the advisory relationship is structured

Bottom Line

A fiduciary retirement advisor should act in your best interest 100% of the time, be paid only by you, and provide retirement focused planning that goes beyond investments. If an advisor cannot explain their fiduciary duty, compensation, risks, and process clearly, they are not the right fit.

If you want to understand how fiduciary retirement planning applies to your situation, schedule an introductory call to review your goals and questions.

Fiduciary Retirement Advisor FAQs

What Is A Fiduciary Retirement Advisor?

A fiduciary retirement advisor is legally required to act in your best interest when providing financial advice, including recommendations, implementation, and ongoing monitoring.

How Can I Tell If An Advisor Is Fee Only?

Ask directly how they are paid and review their Form ADV. Fee-only advisors receive compensation only from client fees and do not earn commissions.

Is Fee-Based The Same As Fee-Only?

No. Fee-based advisors can earn both fees and commissions. Fee-only advisors do not receive any sales related compensation.

Do All CFP® Professionals Act As Fiduciaries?

CFP® professionals are required to follow fiduciary standards when providing financial advice, but you should still confirm how and when that duty applies.

Why Does Fiduciary Status Matter In Retirement?

Retirement decisions are long-term and difficult to reverse. Fiduciary duty helps reduce conflicts and aligns advice with your goals, not product sales.

Reference

Certified Financial Planner Board of Standards. (n.d.). Code of Ethics and Standards of Conduct. Retrieved from https://www.cfp.net/ethics/code-of-ethics-and-standards-of-conduct

Investopedia. (n.d.). Fiduciary. Retrieved from https://www.investopedia.com/terms/f/fiduciary.asp

Financial Industry Regulatory Authority. (n.d.). BrokerCheck. Retrieved from https://brokercheck.finra.org/

Legal Information Institute. (n.d.). Fiduciary duties of trustees. Cornell Law School. Retrieved from https://www.law.cornell.edu/wex/fiduciary_duties_of_trustees

U.S. Securities and Exchange Commission. (n.d.). Staff bulletin: Standards of conduct for broker-dealers and investment advisers care obligations. Retrieved from https://www.sec.gov/about/divisions-offices/division-trading-markets/broker-dealers/staff-bulletin-standards-conduct-broker-dealers-investment-advisers-care-obligations