Your 50s Retirement Reality Check

Retirement feels different when you hit your 50s. What once felt distant starts looking much closer, and the financial decisions you have delayed begin demanding attention.

If you feel behind, you are not alone. The bigger question is not where you should have been years ago. It is what you can still do now to strengthen your retirement future.

The Numbers Deserve A Reality Check

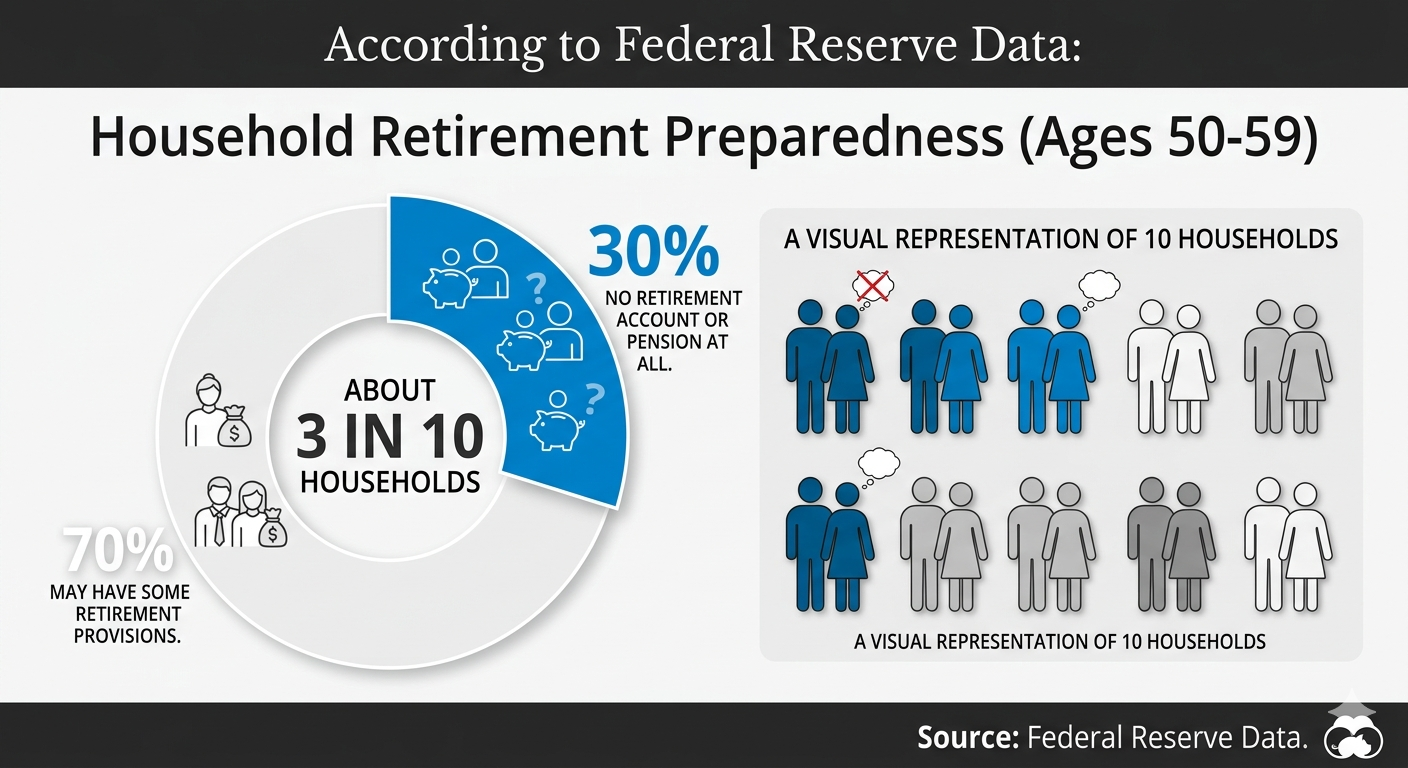

Many Americans in their 50s are approaching retirement with less financial preparation than expected. According to Federal Reserve data in the attached report, about 3 in 10 households led by someone between ages 50 and 59 have no retirement account or pension at all. That is a serious gap, especially when retirement may be only a decade away.

Even those with retirement savings may not be in strong shape. The median retirement account balance for households in their 50s sits around $162,000. On paper, that may sound substantial. In practice, retirement income planning tells a different story.

Retirement Income May Be Smaller Than You Think

A retirement balance is not the same as spendable income.

A $162,000 retirement account may sound reassuring. But using a typical 4% annual withdrawal strategy, that balance may generate only about $6,500 per year.

That shifts the perspective fast.

Social Security helps, but it may not fully close the gap. The attached report shows the average retired worker receives about $2,081 per month, or roughly $25,000 annually.

That could leave a typical single retiree with approximately:

$6,500 from retirement withdrawals

$25,000 from Social Security

~$31,500 total annual income

For households used to higher earnings, that can feel like a major lifestyle adjustment.

Are You Actually Behind?

This question creates stress because people often compare themselves to broad benchmarks without understanding the assumptions behind them. Retirement planning is personal. A business owner, corporate executive, physician, or self-directed investor may all need completely different strategies.

Still, benchmarks can help frame expectations. Fidelity suggests saving six times your salary by age 50, eight times by age 60, and ten times by age 67. If you are not there, that does not automatically mean failure. It means your current trajectory deserves a closer look.

Read: 7 Common Financial Blind Spots for High Earners

Why High Earners Still Fall Behind

Strong income does not automatically create retirement readiness. In fact, higher earners often face a different challenge: lifestyle expansion. As income rises, spending often follows. Larger homes, travel, dining, premium services, and supporting family members can quietly absorb money that should have gone toward retirement.

Many professionals also spend years focused on career building instead of long-term planning. That approach made sense in earlier decades. But in your 50s, the timeline shifts. Waiting for the “right time” to get serious about retirement planning becomes expensive.

Your 50s Still Offer Meaningful Opportunity

The good news is that your 50s still provide real leverage. This is often a high-earning decade, which creates an opportunity to save aggressively if you act with purpose. While your money has less time to grow compared with earlier contributions, stronger contribution rates can still create measurable progress.

The attached report highlights catch-up contributions as one of the most practical ways older workers can accelerate retirement savings. If you have access to tax-advantaged retirement accounts, now is the time to review how much you are contributing and where you may have room to increase.

Also read: Is a Virtual Family Office Right for Your $3M Portfolio?

Employer Matching Still Matters

Some people overlook employer matching because it feels routine. That can be an expensive mistake. Employer contributions represent compensation already available to you, and failing to claim that match leaves money on the table.

The report specifically calls out employer matching as a meaningful strategy for improving retirement outcomes. Even if your broader financial plan needs work, capturing the full match should be one of the easiest immediate wins.

Spending Decisions Shape Retirement Outcomes

Retirement planning is not only about earning more. Sometimes the fastest improvements come from reviewing current spending. Many financially successful professionals know their income but cannot clearly explain where all their monthly cash goes.

This is not about extreme sacrifice. It is about intentional spending. Are recurring costs aligned with your actual priorities? Are convenience habits quietly reducing long-term flexibility? Small adjustments made consistently can redirect meaningful money into retirement accounts over time.

Investment Strategy Needs A Second Look

Some investors become overly conservative as retirement gets closer. That instinct feels understandable, but it can create its own risk. Inflation does not stop in retirement, and portfolios with too little growth potential may struggle to support long term spending needs.

That does not mean taking reckless risks. It means reviewing whether your current investment strategy still aligns with your retirement timeline, comfort with market volatility, and future income goals.

Read: Are You Missing Key Family Tax Opportunities?

DIY Retirement Planning Has Limits

Retirement calculators can be helpful starting points. Rules of thumb can create useful context. But retirement planning becomes more complicated once you move beyond accumulation and start thinking about income distribution.

Questions around tax efficiency, Social Security timing, withdrawal sequencing, healthcare expenses, and spouse coordination require more than generic formulas. This is where many investors realize retirement planning is not simply about building assets. It is about using them wisely.

Avoid Emotional Financial Decisions

People who feel behind sometimes react emotionally. One common mistake is chasing aggressive investments in hopes of making up lost ground quickly. That approach can increase risk at exactly the wrong stage of life.

The opposite mistake is ignoring the issue altogether. Delay reduces flexibility. Assuming Social Security alone will support your preferred retirement lifestyle can also create unrealistic expectations. Better decisions start with honest numbers, not emotional assumptions.

High-Income Professionals Need Strategic Planning

Higher earners often face retirement complexity that basic advice does not address. Larger tax exposure, deferred compensation, investment concentration, business income, and elevated lifestyle expectations all change the planning conversation.

Maxing a retirement account may not be enough. Strategic retirement planning often requires coordinated decisions across tax planning, investment management, withdrawal sequencing, and long-term income design. This is often where professional financial guidance becomes especially useful.

How A Virtual Family Office Helps

If you feel behind on retirement, trying to solve everything alone can make the problem feel bigger than it is. A virtual family office gives you structured financial guidance without the complexity of managing every moving part yourself.

Instead of focusing only on investments, a virtual family office looks at your full financial picture. That can include retirement income planning, tax strategies, Social Security timing, healthcare costs, estate planning coordination, and long-term cash flow management.

For pre-retirees in their 50s, this kind of support can help turn uncertainty into a practical plan. Rather than guessing what to do next, you have a clearer framework built around your goals, timeline, and financial reality.

Bottom Line

Retirement planning is not about getting everything perfect. It is about making smarter decisions with the time and resources you still have.

Even if your savings are not where you hoped they would be, meaningful progress is still possible. The right strategy can help you close gaps, avoid costly mistakes, and build a more confident path toward retirement.

If you want a clearer plan for your next chapter, One Advisory Partners can help you create a retirement strategy built around your life, not generic assumptions.

FAQs

Is It Too Late To Start Retirement Planning In Your 50s?

No. Starting earlier helps, but your 50s still offer time to improve retirement outcomes through stronger savings, better planning, and smarter financial decisions.

How Much Should I Have Saved By Age 50?

Some planning guidelines suggest around six times your annual salary by age 50. Your actual target depends on your expected retirement lifestyle, expenses, and other income sources.

Can Social Security Fully Replace My Income?

For most people, no. Social Security can provide foundational retirement income, but many households need additional assets to maintain their preferred lifestyle.

Should High-Income Earners Work With A Financial Planner?

Often yes. Higher income can create more complexity involving taxes, investments, retirement distribution planning, and long-term income strategy.

What Should I Do First If I Feel Behind?

Start with a full financial review. Assess retirement balances, spending, debt, projected retirement age, and expected income sources. Clear numbers create better decisions.

References

Federal Reserve Board. (n.d.). Survey of Consumer Finances (SCF). Retrieved from https://www.federalreserve.gov/econres/scfindex.htm

Investopedia. (n.d.). Even in their 50s, many Americans have no retirement account or pension. Retrieved from https://www.investopedia.com/even-in-their-50s-many-americans-have-no-retirement-account-or-pension-11966501

Social Security Administration. (n.d.). Monthly statistical snapshot. Retrieved from https://www.ssa.gov/policy/docs/quickfacts/stat_snapshot/

Fidelity. (n.d.). Average retirement savings by age: Are you normal? Retrieved from https://www.fidelity.com/learning-center/personal-finance/average-retirement-savings