What Are the 7 Tax Filing Mistakes Retirees Make That Cost the Most?

Tax filing mistakes retirees make can quietly drain your retirement income. You stop earning a paycheck, but your taxes do not stop. They shift.

Instead of one income source, you now manage several. Social Security. Retirement accounts. Investments. Maybe part-time work. Each one follows different tax rules. The way they interact can push you into higher tax brackets, increase Medicare premiums, or trigger penalties.

Here are 7 tax filing mistakes retirees make and how to avoid them.

1. Missing Required Minimum Distributions

Required minimum distributions begin at age 73 or age 75 for most traditional retirement accounts. Once you reach that point, the IRS requires you to withdraw a specific amount each year. Missing that requirement can lead to penalties on the amount not withdrawn.

This often happens when accounts are spread across multiple institutions or older accounts are overlooked. It is not always a calculation issue. It is usually a visibility issue, where no single system tracks everything.

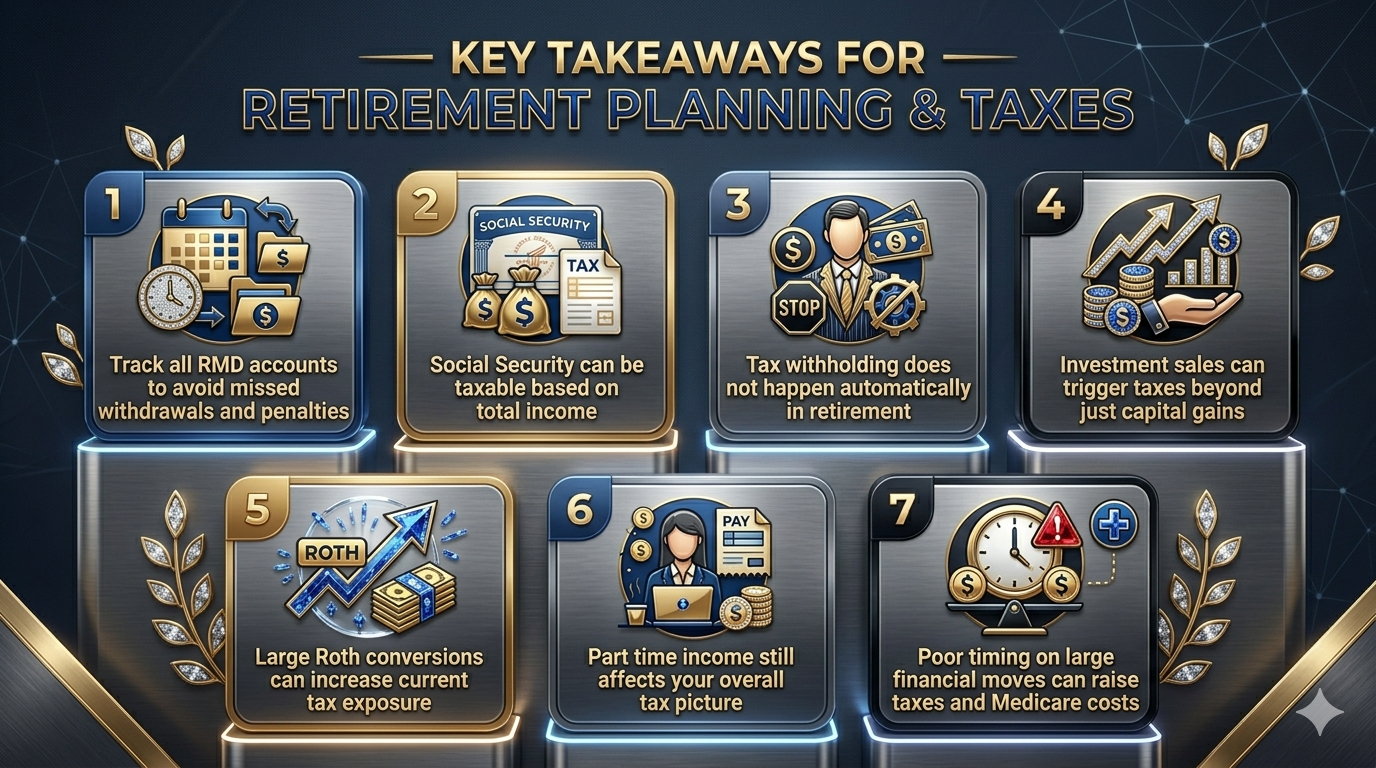

What to do instead: Track every RMD-eligible account in one place and review required amounts before year-end. Align withdrawals with your broader tax strategy, not just compliance.

Read: Top 10 Common RMD and Withdrawal Mistakes for Raytheon Retirees

2. Underestimating Social Security Taxes

Many retirees assume Social Security is tax-free. In reality, a portion of your benefits can become taxable depending on your total income. Withdrawals from retirement accounts, pensions, and investment income all factor into that calculation.

The impact builds quickly. A single withdrawal can increase your total income, which then increases how much of your Social Security is taxed. This creates a layered effect that often goes unnoticed until filing.

What to do instead: Coordinate withdrawals with your total income to manage how much of your benefits become taxable. Keep income levels steady to avoid unnecessary tax spikes.

Read: How Social Security Works After Your Spouse Dies

3. Letting Withholding Fall Through the Cracks

During your working years, taxes are handled through payroll withholding. That structure disappears in retirement. Many income sources either withhold too little or nothing at all unless you request it.

This gap usually shows up at filing. A larger-than-expected balance due or an underpayment penalty. It is not caused by one mistake, but by a lack of planning across income sources.

What to do instead: Project your annual tax liability early and adjust withholding across income sources. Use estimated payments to stay ahead instead of catching up later.

4. Treating Investment Decisions Separately From Taxes

Selling investments can generate capital gains that increase your taxable income. That increase does more than affect your tax bracket. It can also impact Social Security taxation and future Medicare premiums.

When multiple sales happen in the same year, income stacks. This creates a chain reaction across your entire return. Without planning, even necessary portfolio changes can lead to higher taxes than expected.

What to do instead: Evaluate the tax impact before selling any asset and plan transactions across multiple years. Manage gains and losses intentionally to control total taxable income.

5. Converting Too Much to a Roth IRA at Once

Roth conversions can reduce future tax exposure by moving assets into a tax-free structure. However, the amount converted is treated as taxable income in the year it happens.

Large conversions can push you into a higher tax bracket and increase the taxable portion of your Social Security. They can also affect future Medicare premiums, even if the connection is not immediately visible.

What to do instead: Spread conversions across several years to stay within a target tax range. Time each conversion based on your full income picture, not just account size.

Also read: What Does the One Big Beautiful Bill Act (OBBBA) Really Mean for You?

6. Overlooking Income From Part-time Work

Many retirees continue to earn income through consulting, freelance work, or part-time roles. While this income may seem minor, it still affects your overall tax picture.

Earned income can increase the taxable portion of Social Security and may also introduce additional tax obligations. When it is not tracked or planned for, it creates avoidable surprises.

What to do instead: Include all income streams in your tax planning from the start. Track earnings and set aside taxes as you go to avoid surprises.

7. Poor Timing Around Large Financial Moves

Large financial decisions such as selling a home, liquidating investments, or taking significant withdrawals can shift your tax situation in a single year. These moves often increase taxable income more than expected.

Without planning, one transaction can affect multiple areas of your return. It can raise your tax bracket, increase Social Security taxation, and impact future Medicare costs.

What to do instead: Review the tax impact before any major transaction takes place. Time large gains carefully to reduce ripple effects across your return.

Why A Virtual Family Office Works

Most tax mistakes in retirement do not come from lack of knowledge. They come from lack of coordination.

A Virtual Family Office brings every moving part into one system. Investments, taxes, retirement income, and estate planning all work together. Instead of making isolated decisions, every move is reviewed based on its full impact.

That changes outcomes. Withdrawals are timed with tax brackets. Investment decisions factor in tax consequences. Income is structured to avoid unnecessary spikes. The result is fewer surprises and more control over your financial life.

How ONE Advisory Partners Can Help You

At ONE Advisory Partners, the focus is not just on managing investments. The goal is to coordinate every part of your financial life through a Virtual Family Office approach.

This means your tax strategy, income plan, and investment decisions are aligned from the start. Instead of reacting at tax time, planning happens throughout the year. That allows you to reduce avoidable taxes, manage Medicare exposure, and make more informed financial decisions.

Bottom Line

Tax filing mistakes retirees make are rarely about missing information. They come from decisions made in isolation.

When income, taxes, and investments are managed together, you gain more control over how your retirement income is taxed. That is where better outcomes start.

Common Questions About Retirement Tax Mistakes

What are the most common tax filing mistakes retirees make?

Missing RMDs, underestimating Social Security taxes, not adjusting withholding, and poorly timing withdrawals or investment sales. These usually happen when income sources are not coordinated.

Do retirees still need to pay taxes after retirement?

Yes. Income from Social Security, retirement accounts, pensions, and investments can all be taxable depending on how they combine.

How can retirees reduce taxes on Social Security?

Manage your total income. Coordinate withdrawals and avoid large spikes that increase the taxable portion of your benefits.

What happens if you miss an RMD?

You may face a penalty on the amount not withdrawn. You may also increase future taxable income when correcting it.

Are Roth conversions a good strategy in retirement?

Yes, but timing matters. Large conversions in one year can raise your tax bill and affect other areas like Social Security and Medicare.

Do retirees need to pay quarterly taxes?

Sometimes. If withholding is not enough, estimated quarterly payments help avoid penalties.

How does a Virtual Family Office help reduce taxes?

It aligns income, investments, and tax planning into one strategy, helping you control timing and reduce unnecessary tax exposure.

Reference

Internal Revenue Service. (2025). Retirement plan and IRA required minimum distributions FAQs. Retrieved from https://www.irs.gov/retirement-plans/retirement-plan-and-ira-required-minimum-distributions-faqs

Internal Revenue Service. (2025). Publication 915: Social Security and equivalent railroad retirement benefits. Retrieved from https://www.irs.gov/publications/p915

Internal Revenue Service. (2025). Publication 505: Tax withholding and estimated tax. Retrieved from https://www.irs.gov/publications/p505

Internal Revenue Service. (2025). Topic No. 404: Dividends and other corporate distributions. Retrieved from https://www.irs.gov/taxtopics/tc404

Internal Revenue Service. (2025). Topic No. 409: Capital gains and losses. Retrieved from https://www.irs.gov/taxtopics/tc409

Investopedia. (2026). 6 tax filing mistakes retirees make and how to avoid them. Retrieved from https://www.investopedia.com/6-tax-filing-mistakes-retirees-make-and-how-to-avoid-them-11917840

Internal Revenue Service. (2025). Topic No. 403: Interest received. Retrieved from https://www.irs.gov/taxtopics/tc403

Internal Revenue Service. (2025). Self-employed individuals tax center. Retrieved from https://www.irs.gov/businesses/small-businesses-self-employed/self-employed-individuals-tax-center

Internal Revenue Service. (2025). Topic No. 701: Sale of your home. Retrieved from https://www.irs.gov/taxtopics/tc701

Social Security Administration. (2026). Medicare premiums and income-related adjustments. Retrieved from https://www.ssa.gov/benefits/medicare/medicare-premiums.html