What Is Gray Divorce and Why Does It Carry Greater Financial Risk?

Gray divorce is rising, and gray divorce brings different emotional and financial pressures than earlier life divorce. After 50, you do not just divide assets. You divide retirement plans, healthcare coverage, and decades of shared history.

Here is what makes gray divorce different and the financial mistakes you need to avoid.

What Is Gray Divorce?

Gray divorce refers to divorce that happens after age 50. The term reflects the growing number of older couples who choose to separate later in life.

Unlike earlier divorces, gray divorce often occurs after children are grown and major assets have already been built. Instead of focusing on custody and child support, you focus on dividing retirement accounts, pensions, property, and long term income sources.

What Changes Emotionally After 50?

When younger couples divorce, they often focus on raising children in two households. Over 50, children are usually adults. They can weigh in, take sides, and sometimes focus on inheritance rather than reconciliation.

Gray divorce can also feel isolating. Your identity may tie closely to a long term marriage. Shared routines, friendships, and retirement dreams suddenly dissolve. You do not just lose a spouse. You lose a future you assumed was secure.

How Does Retirement Planning Shift?

Younger spouses have decades of earning power ahead. They can rebuild savings, shift careers, and recover from market downturns. After 50, you often stand near retirement or already live on a fixed income.

Most assets are already accumulated. The key question becomes simple and direct: Can each of you live independently on your share? There is less margin for error and less time to correct mistakes.

Why Does Income Drop Hit Harder?

Living alone costs more than sharing expenses. Mortgage payments, utilities, property taxes, and insurance no longer split between two people. You may also lose access to your spouse’s health care coverage.

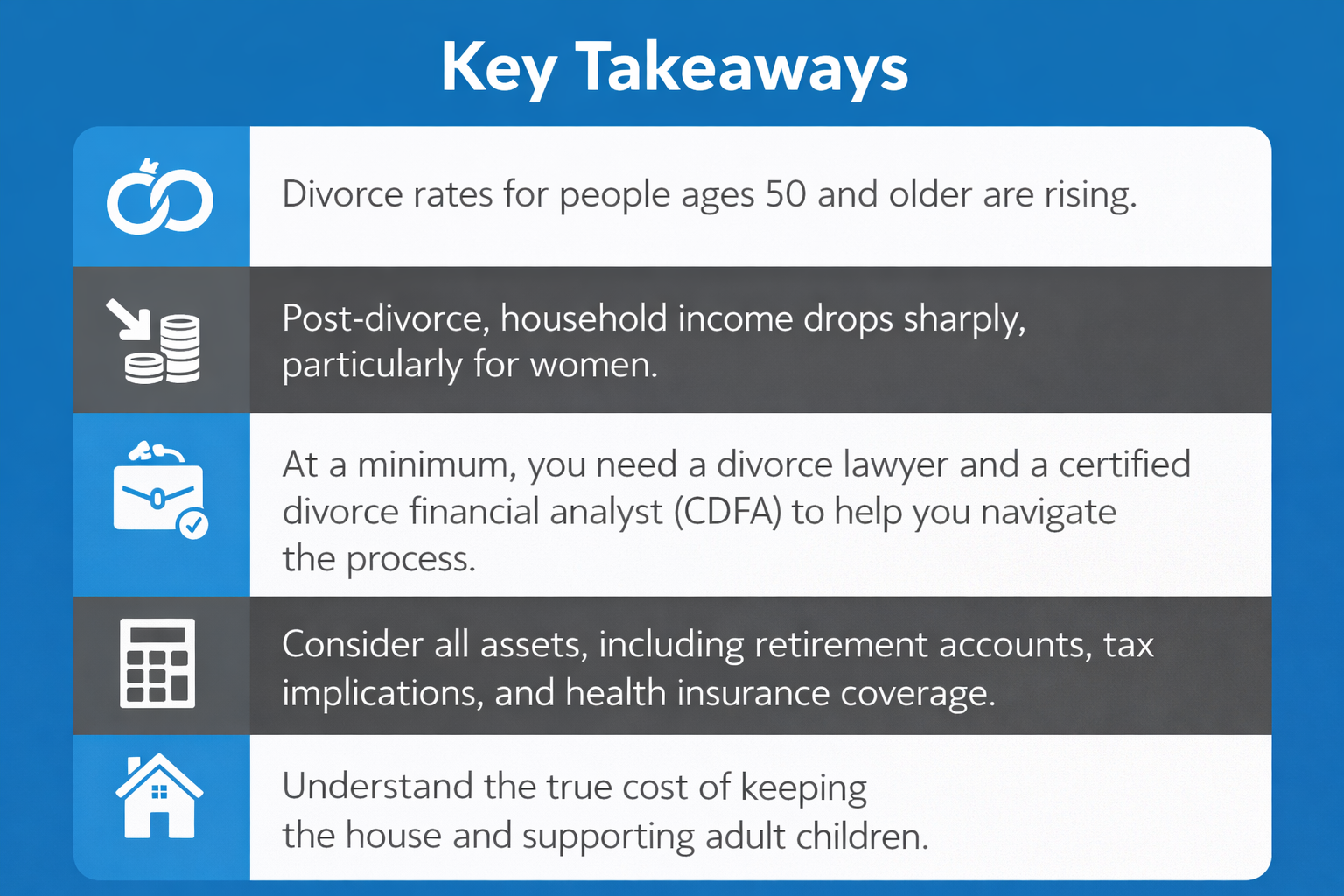

Women often feel the impact more sharply. Many recently divorced women experience significant income declines. Women also tend to live longer, which stretches fewer resources over more years.

Gray divorce can shatter retirement projections overnight.

How Do Healthcare and Long-Term Care Factor In?

Divorcing before age 65 can leave you scrambling for coverage. If you relied on your spouse’s employer sponsored plan, you must secure your own insurance through work, the Affordable Care Act exchange, or COBRA.

Health care costs rise with age. Chronic illness, cognitive decline, and long term care needs add pressure. In gray divorce, you must plan for medical risk alone, not as a couple.

What Happens to Pensions and Social Security?

Pensions earned during marriage usually count as joint assets. You may split future payments or offset the present value. The method you choose can change your monthly income for decades.

If you are 62 or older, you may qualify for Social Security benefits based on your former spouse’s record under certain rules. Many people overlook this option, which can provide meaningful support.

Gray divorce forces you to understand every income stream.

10 Financial Mistakes to Avoid in a Gray Divorce

Gray divorce requires precision. These common errors can derail your financial future.

1. Failing to List Every Asset

One spouse often manages the finances. If that was not you, gather full documentation before negotiations begin.

Include:

Bank accounts

Brokerage accounts

Retirement plans

Pensions

Life insurance policies

Real estate

Business interests

You cannot divide what you do not track.

2. Keeping the House Without Running the Numbers

The family home feels stable. It may also drain your cash. You must calculate mortgage costs, property taxes, insurance, and repairs.

Ask yourself if one income can sustain it long term. Sentiment should not override math.

3. Ignoring Debt Exposure

You may owe part of your spouse’s debt, especially in community property states.

Pull credit reports for both parties. Confirm balances. Address liabilities before finalizing agreements.

4. Overlooking Tax Consequences

Every asset carries tax implications. A brokerage account with gains brings a tax bill. Retirement accounts carry withdrawal rules.

Consult a tax professional before choosing lump sum payments or transferring accounts. Small decisions can create large tax exposure.

5. Mishandling Retirement Transfers

If you withdraw funds from an IRA before age 59½, you face a penalty.

A qualified domestic relations order allows certain one time transfers from employer plans without penalty. Structure this carefully to avoid unnecessary loss.

6. Failing to Plan for Health Insurance

Divorce can end employer sponsored coverage. COBRA can extend coverage up to 36 months but often at higher cost.

Price out your options before signing agreements.

7. Supporting Adult Children at the Expense of Retirement

You may feel compelled to help adult children. But draining retirement savings puts your own stability at risk.

Secure your financial base first.

8. Hiding Assets

Attempting to conceal assets can result in penalties, settlement changes, or fraud charges.

Transparency protects you legally and financially.

9. Underestimating Post Divorce Expenses

Your income will likely shrink. Expenses may stay the same or rise.

Create a detailed budget that reflects housing, healthcare, insurance, food, transportation, and taxes.

10. Building the Wrong Advisory Team

Gray divorce requires professionals. At minimum, consider a divorce attorney and a certified divorce financial analyst.

Strong advice can reduce costly errors and protect long term income.

How ONE Advisory Partners Helps

Gray divorce requires more than dividing accounts. You need a coordinated plan that protects retirement income, manages taxes, and addresses health care and estate planning risks. ONE Advisory Partners takes a holistic, long term approach so you can see the full picture before making major decisions.

The team helps you organize assets, evaluate pension and Social Security strategies, review tax exposure, and create a sustainable post divorce income plan. Instead of reacting to short term pressure, you move forward with a structured, well defined plan built around long term stability and financial independence.

The Bottom Line

Gray divorce is different because time, health, and income stability matter more. You are not planning for college funds. You are protecting retirement income, healthcare access, and estate intentions.

If you approach gray divorce with clarity and discipline, you can protect your independence and build a secure next chapter.

Gray Divorce FAQs

What is gray divorce?

Gray divorce refers to divorce after age 50. It often involves dividing retirement assets instead of dealing with child custody.

Why is gray divorce increasing?

People live longer, have more financial independence, and feel more willing to leave unhappy marriages later in life.

How does gray divorce affect retirement?

You divide savings, pensions, and investments built over decades. You also lose shared living expenses, which can strain retirement income.

Can I collect Social Security from my ex spouse?

You may qualify if the marriage lasted at least 10 years and you meet age requirements. Your claim does not reduce your ex spouse’s benefit.

What happens to pensions?

Pensions earned during marriage usually count as marital property. Courts may split future payments or offset their present value.

Should I keep the house?

Only if you can afford the mortgage, taxes, insurance, and upkeep on one income. Run the numbers before deciding.

How does gray divorce impact health insurance?

If you relied on your spouse’s plan, you must secure your own coverage through work, the ACA marketplace, or COBRA.

Is alimony common in gray divorce?

It can be, especially in long term marriages where one spouse earned significantly less.

Do adult children affect decisions?

They can influence emotions and estate planning, but your retirement security must come first.

Reference

Forbes. (2025, February 13). Gray divorce: Divorcing over age fifty. Retrieved from https://www.forbes.com/sites/patriciafersch/2025/02/13/gray-divorce-divorcing-over-age-fifty/

Bowling Green State University. (2024, October). BGSU research finds divorce among older adults has nearly tripled since 1990. Retrieved from https://www.bgsu.edu/news/2024/10/bgsu-research-finds-divorce-among-older-adults-has-nearly-tripled-since-1990.html

U.S. Census Bureau. (2023, July). Marriage and divorce rates. Retrieved from https://www.census.gov/library/stories/2023/07/marriage-divorce-rates.html

U.S. Census Bureau. (2021). Marriages and divorces: Press release. Retrieved from https://www.census.gov/newsroom/press-releases/2021/marriages-and-divorces.html

Internal Revenue Service. (n.d.). Publication 504: Divorced or separated individuals. Retrieved from https://www.irs.gov/publications/p504

Investopedia. (n.d.). Mistakes to avoid when divorcing over 50. Retrieved from https://www.investopedia.com/personal-finance/mistakes-avoid-when-divorcing-over-50/