Your Divorce Financial Checklist Before You File

Divorce forces you to make financial decisions at the same time your life is changing. Income may shift, expenses may rise, and access to accounts can become limited. If you are not prepared, it is easy to rely on incomplete information or react under pressure.

This article is your divorce financial checklist before you file. It walks you through the key steps to organize your finances, protect your position, and plan your next move with clarity. Each section builds on the last so you can move forward with a structured plan instead of guesswork.

Build Your Financial File First

Start by gathering every financial document tied to you and your spouse. This includes tax returns, bank statements, investment accounts, retirement funds, insurance policies, and debt records. You want a complete view of your financial life before anything changes.

Without documentation, you rely on estimates or what your spouse shares. That creates risk. Store copies securely using password-protected files or a safe location. The goal is to have full access to your financial data before the process begins.

Read: Should You Keep the House After Divorce?

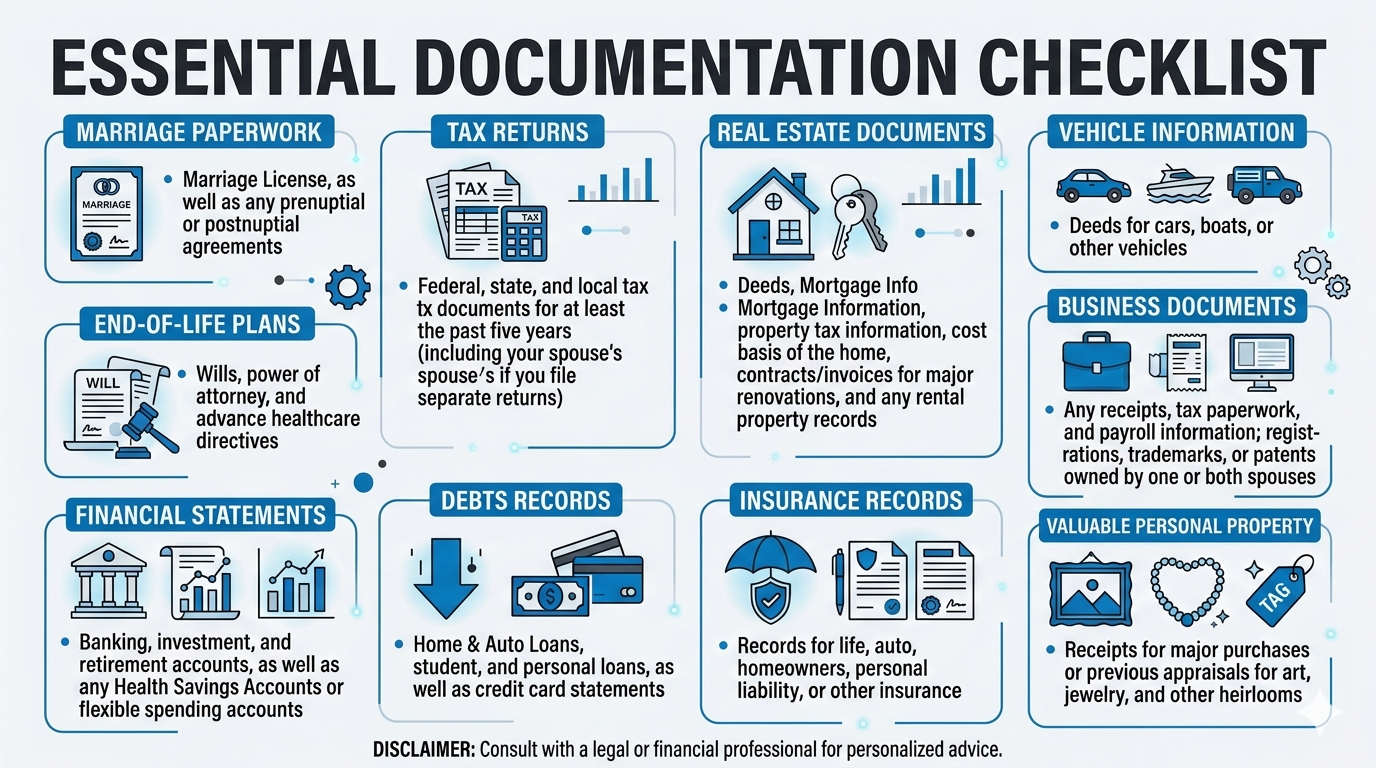

Organize Your Financial Management System

Once documents are collected, organize them into a system you can use. Create folders by category so you can find anything quickly. This reduces delays and helps you stay in control during discussions or legal review.

Include categories like marriage records, tax filings, real estate, business records, financial accounts, debts, insurance, and personal property. A structured system turns your documents into usable information, not just stored files.

Map Your Real Monthly Spending

Track your actual spending using bank and credit card statements. Break it into categories like housing, food, transportation, childcare, insurance, and personal expenses. This gives you a clear picture of your lifestyle.

This step helps you understand what you need after divorce. It also supports financial discussions if you need to justify your expenses. Without real numbers, it becomes difficult to plan your next phase.

Separate Your Financial Access

Open accounts in your name if you do not already have them. Set up a checking account, savings account, and a credit card. Start directing your income into your personal account to build financial independence.

Avoid transferring large amounts from joint accounts without advice. That can create legal issues. Focus on creating separation moving forward while keeping your actions reasonable and documented.

Audit Your Credit And Debt Exposure

Pull your credit report and review every account. Look for joint debts, unknown liabilities, and any accounts where you are listed as an authorized user. This step shows your full financial exposure.

You are still responsible for joint debt unless it is clearly assigned later. Monitoring your credit helps you avoid surprises and prepares you for negotiations. It also helps you protect your credit during the process.

Also read: What Is Gray Divorce and Why Does It Carry Greater Financial Risk?

Identify And Value Everything You Own

List all assets and estimate their value. Include real estate, retirement accounts, investments, business interests, vehicles, and high-value personal items. Some assets may require professional valuation.

Do not assume equal value across assets. Liquidity, taxes, and timing all affect what an asset is actually worth to you. Understanding this helps you make better decisions during settlement discussions. If you want to keep the family home, work with a Certified Divorce Lending Professional (CDLP) to see if you can qualify to assume or refinance the mortgage on your own before you sign any divorce settlement

Break Down Income From All Sources

Gather details on all income streams. This includes salary, bonuses, business income, commissions, and any stock-based compensation. Also review benefits like retirement contributions or employer perks.

Accurate income data is critical for financial planning and support calculations. If income is unclear or incomplete, your position becomes weaker. Collect this information early while access is still available. Don't forget about digital assets such as ApplePay, Venmo, PayPal, and Crypto. You can run your credit report free once a year at www.annualcreditreport.com.

Define Your Income Potential

Assess your ability to earn income on your own. Look at your current skills, work history, and opportunities in your field. If needed, consider additional training or certification.

This step shapes your financial independence and long-term plan. It affects your budget and your reliance on support. Understanding your earning potential helps you plan realistically for life after divorce.

Factor In Taxes Before Making Decisions

Review the tax impact of each asset. Retirement accounts may be taxed on withdrawal, while other assets may carry capital gains or different tax treatment. Not all assets are equal after taxes.

A balanced split on paper may not be equal in reality. Focus on after tax value when evaluating options. This helps you avoid decisions that reduce your long-term financial position.

Also read: Are Women Paying the Price for Divorce?

Plan For Health Insurance Gaps

If you rely on your spouse’s health insurance, you will need a replacement. Review options such as employer plans, private coverage, or temporary continuation coverage.

Health insurance can become a major monthly expense. Include it in your budget early so it does not create pressure later. Planning ahead helps you avoid gaps in coverage and unexpected costs.

Work With Professionals Early

Consult professionals before filing. This may include a divorce attorney, financial advisor, tax professional, and therapist. Each plays a role in helping you make informed decisions.

Early advice helps you avoid mistakes and build a stronger strategy. Waiting until later can limit your options and increase stress during the process.

Protect Yourself From Financial Risk

If access to money is limited or monitored, take steps to protect yourself. Open separate accounts, secure documents, and update passwords on personal accounts.

Document any unusual financial behavior. This can support your position if disputes arise. Protecting your access and information helps you stay in control throughout the process.

Plan Your Post-Divorce Life

Think about your financial life after divorce. Decide where you will live, what your priorities are, and what stability looks like for you.

Clear goals help guide your decisions. When you know what you want your future to look like, it becomes easier to evaluate options and negotiate effectively.

How A Virtual Family Office Helps

A Virtual Family Office brings your financial strategy into one coordinated plan. Instead of working with separate advisors, it aligns investments, taxes, estate planning, and cash flow in one place.

This coordination matters during divorce. Decisions in one area affect everything else. With a unified approach, you can evaluate options based on long-term outcomes instead of short-term tradeoffs.

The Bottom Line

Your divorce financial checklist before you file is about preparation and control. When your finances are organized and your plan is clear, you can make decisions that support your long-term stability.

If you want a coordinated strategy across investments, taxes, and long-term planning, connect with ONE Advisory Partners to build a plan that supports your next chapter.

FAQs

When Should I Start Financial Planning Before Divorce?

Start as soon as divorce becomes a possibility. Early preparation gives you time to gather information and build a strategy without pressure.

Waiting limits access and increases risk. Acting early gives you more control over your financial decisions.

Can My Spouse Move Money Before I File?

Yes, unless there is a legal restriction. This is why separating accounts and tracking finances early is important.

If it happens, document everything. This may be addressed later during settlement.

Do I Need Both A Lawyer And A Financial Advisor?

Yes. A lawyer handles legal structure while a financial advisor helps you understand long-term impact.

Both roles are important for building a complete strategy and avoiding costly mistakes.

Will Divorce Affect My Credit?

Divorce does not directly affect your credit score. However, missed payments or joint debt issues can impact it.

Monitoring your credit and staying current on payments helps protect your financial standing.

What Is The Biggest Mistake Before Divorce?

The biggest mistake is waiting too long to prepare. Rushed decisions often lead to poor outcomes.

Early planning gives you clarity, control, and better options during the process.

Reference

Internal Revenue Service. (n.d.). Tax considerations for people who are separating or divorcing. Retrieved from https://www.irs.gov/newsroom/tax-considerations-for-people-who-are-separating-or-divorcing

Investopedia. (n.d.). Divorce planning checklist: What you need to know. Retrieved from https://www.investopedia.com/articles/personal-finance/093015/divorce-planning-checklist-what-you-need-know.asp

Charles Schwab. (n.d.). Financial steps to prioritize during divorce. Retrieved from https://www.schwab.com/learn/story/financial-steps-to-prioritize-during-divorce

Justia. (n.d.). First steps for divorce. Retrieved from https://www.justia.com/family/divorce/first-steps-for-divorce/